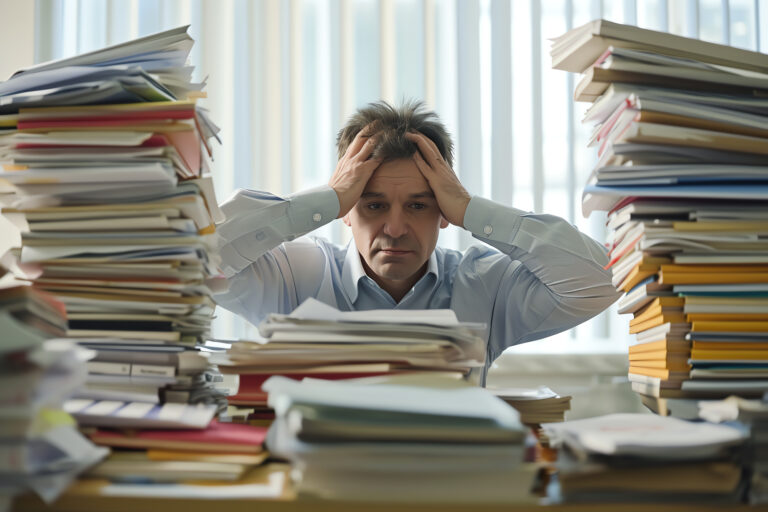

Even before this year’s economic turmoil, financial anxiety was already gripping Americans at alarming levels. A Discover survey from last year revealed that four out of five Americans were worried about their financial situation. Top concerns included inflation, rising everyday expenses, and general uncertainty in the economy.

How to Cope With Financial Anxiety During Economic Uncertainty

Fast forward to today, and the picture hasn’t improved. With tariffs, a looming global trade war, and volatile markets (the S&P 500 is down about 9% year-to-date), financial fear is intensifying. According to Megan McCoy, a financial therapist and associate professor at Kansas State University, “Since Covid, we’ve all just been waiting for the next shoe to drop, moneywise. We can’t catch our breath.”

Unfortunately, this anxiety can become a self-fulfilling prophecy. Financial stress is linked not only to mental health issues like depression and Financial anxiety, but also to physical ailments such as high blood pressure and even heart attacks. Worse, fear-driven decisions often worsen long-term financial well-being.

If you’re feeling the pressure, here are six expert-backed strategies to help protect your finances and your mental health.

1. Adjust Your Perspective

It’s easy to get caught up in the daily swings of the stock market. For instance, in one recent week, the S&P 500 saw a dramatic 10.5% two-day drop—followed by a 9.5% one day gain. These sharp ups and downs fuel panic, but financial psychologist Dr. Brad Klontz reminds us to zoom out. “What feels like a cliff in the short term is usually just a speed bump long term,” he says.

Historically, the stock market has averaged 10% annual returns over the last century. Whether you’re still decades from retirement or already there, the long-term outlook still favors growth.

Tip: Compare your 401(k) to your balance from a year or five years ago—not its all-time high. This reframes your perspective and helps reduce fear-based decisions.

2. Slow Your Roll

When markets drop, the impulse to sell and protect what’s left is strong. In Q1 2025, 401(k) trading volume hit a five-year high, with most trades happening on days of market chaos. This kind of reactive behavior often leads to selling low—and missing the rebound.

Dr. Naomi Win, a behavioral analyst, suggests a simple rule: Wait one hour before making any financial decision. Set a timer. Use that time to reach out to a financial advisor or a trusted friend with a calm head.

This helps bypass the brain’s “fight-or-flight” response, giving your prefrontal cortex time to re-engage so you can make rational choices instead of emotional ones.

3. Stop Checking Your Balances (Seriously)

Thanks to a cognitive bias called loss aversion, seeing a drop in your account balance hurts far more than seeing gains brings joy. And the more frequently you check, the more likely you’ll feel that pain.

Behavioral economists Shlomo Benartzi and Richard Thaler found that infrequent checkers earn significantly higher returns over time. That’s because they’re less likely to panic-sell during a dip.

Pro tip: Check your portfolio no more than once a quarter, or even just once a year. You’ll make calmer, better decisions that way.

Also, limit your exposure to economic news. When everyone around you is panicking, it’s much harder to stay calm yourself.

4. Imagine the Worst (So You Can Prepare)

This sounds counterintuitive, but thinking through your worst-case financial scenario can actually be empowering. Worried about losing your job? Start by calculating how long your emergency fund would last. Then, brainstorm next steps: Could you cut expenses, move to a cheaper place, or reach out to your network?

“Having a plan in place—even one you never use—reduces anxiety,” says Dr. Win.

5. Focus on One Action You Can Control

You can’t control inflation, the market, or recession—but you can control your own financial habits.

- Start building or replenishing your emergency fund

- Cut discretionary spending (subscriptions, takeout, travel)

- Upskill in your field to boost job security

- Network or begin a side hustle for extra income

Taking even one productive step can offer a strong sense of control, which reduces financial stress.

Bonus Tip: Look for areas outside of money to take control—organize your closet, clean your office, take a walk. These activities provide small wins that make you feel better overall.

6. Practice Self-Compassion

It’s natural to blame yourself for financial trouble. Maybe you feel like you should have saved more or invested differently. But remember: You were doing the best you could with the information you had at the time.

Dr. McCoy encourages gentle reframing. “This isn’t a personal failure. It’s a collective one. You are not alone.”

Accepting your mistakes with kindness—and learning from them—is more powerful than beating yourself up.

Financial Anxiety and Mental Health: A Vicious Cycle

Financial anxiety doesn’t just impact your wallet—it affects your mental health, too. Chronic money-related stress has been linked to:

- Anxiety disorders

- Depression

- Insomnia

- Burnout

- Headaches and heart disease

Addressing financial anxiety requires both practical strategies and emotional support. If you feel overwhelmed, talking to a therapist—especially one trained in financial therapy—can help you build resilience and reclaim peace of mind.

Frequently Asked Questions (FAQ)

What is financial anxiety?

Financial anxiety is a feeling of worry, fear, or stress about money. It can stem from debt, job loss, market downturns, or broader economic uncertainty.

How does financial anxiety affect mental health?

Prolonged Financial anxiety can lead to anxiety disorders, depression, sleep issues, and chronic health problems. It can also reduce your ability to make rational decisions, compounding financial issues.

Should I talk to a professional about my money anxiety?

Absolutely. Financial planners can help you make better money decisions, while therapists—especially financial therapists—can help you understand and manage the emotions behind those decisions.

How often should I check my 401(k) or retirement account?

Experts suggest checking once a quarter or even once a year. Checking too frequently increases your chances of reacting emotionally to short-term market movements.